2:34

Hear from our Chairman and Senior Partner, Kevin Ellis

Welcome to our first digital Transparency Report

Whilst PwC is a multidisciplinary firm, this report is primarily focused on our Audit practice and related services. It will be of particular interest to the investor community and Audit Committee members and chairs.

Hear from our Chairman and Senior Partner, our Head of Audit, and Chair of our Public Interest Body as they reflect on the last year and look ahead on our continuing journey to enhance audit quality.

Welcome to our first digital Transparency Report

An update on our Programme to Enhance Audit Quality

Considering the public interest aspects of the firm’s work

The quality control system for our Audit practice as explained within our Transparency Report, has been suitably designed and complied with. The quality control system provides us with reasonable assurance that we perform and report in line with applicable professional standards.

We have had an encouraging set of inspection results this year, and continue to invest in our Programme to Enhance Audit Quality (PEAQ). By evolving our system of quality control, we will ensure it remains fit for purpose in a changing environment.

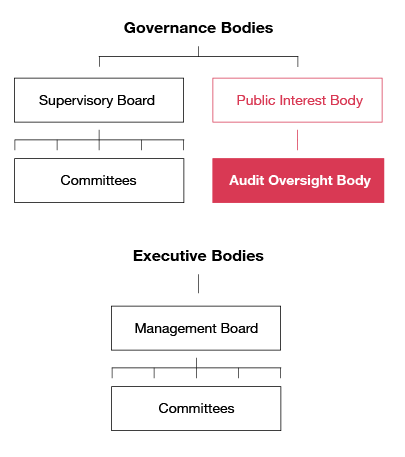

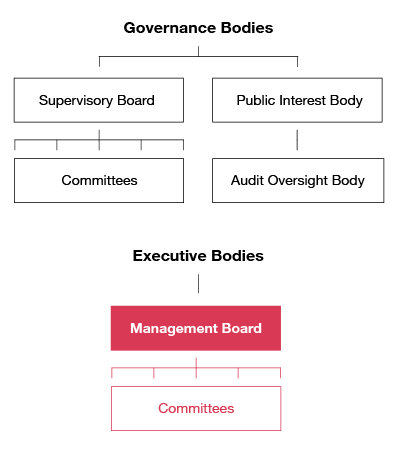

The firm’s governance is guided by our purpose – to build trust in society and solve important problems. Our purpose is central to our decision making processes and our risk appetite. It also informs how we manage our business in the interests of our partners and stakeholders.

The key matters considered in the year by our governance bodies included strategy, culture, people, quality, performance, regulation and reputation. The governance of key risks facing the firm (including cyber, regulatory and litigation risks) were also considered by the firm’s governance bodies.

The key governance bodies of the firm are described below.

The Supervisory Board (‘SB’) considers a wide range of issues such as risk, strategy, reputation, people matters including health and wellbeing, technology, return on investments, and culture. It has supported, given guidance to and challenged the Chairman and Senior Partner and the Management Board. The SB has particular insight on the views of partners and reflects these in conversations with management.

This is a modal window.

"I am delighted to Chair the Audit Oversight Body at a time when audit quality, audit culture, and the audit profession as a whole remain under the spotlight."

View TranscriptThe following documents provide additional detail on the firm’s governance

Objectivity is the hallmark of our profession, at the heart of our culture and fundamental to everything we do. Independence underpins objectivity and has two elements: independence of mind and independence in appearance. We take ethical behaviour seriously. We embrace the spirit and not just the letter of the relevant ethical requirements.

This is a modal window.

The firm’s Ethics partner is Nicola Shield, and the firm’s Partner Responsible for Independence is Jon Walters. Nicola and Jon are supported by a team of specialists who help ensure that policies and processes are comprehensively and consistently applied.

View TranscriptThis document provides additional detail on the firm’s independence and ethics policies, procedures and tools

We aim to attract, develop, reward and retain top talent by creating a culture where the best people want to stay and build their careers.

We have a focused recruitment and onboarding strategy and have continued to recruit and onboard throughout the pandemic. Having the right people with the right skills is fundamental to audit quality.

Our main priority throughout the pandemic has been our people - and in particular, their wellbeing and job security. During the worry and uncertainty, we’ve sought to provide reassurance, care and clarity, and our consistently high engagement scores over the last year reflect this.

As well as protecting jobs, we’ve been able to make an unprecedented investment in our people, while planning for a post-pandemic world, continuing recruitment activity and investing in the workforce of the future.

The ability to challenge and apply professional scepticism is key to delivering high quality audits. At the start of the PEAQ we commissioned an independent paper from Professor Karthik Ramanna on “Building a culture of challenge in audit firms”.

We used this independent perspective, along with PwC’s cultural experts in our People and Organisation team, to review our culture and develop our “critical few” Audit behaviours to drive high quality:

This behaviour means being inclusive and working together, encouraging a ‘problem shared’ ethos, investing in personal and professional development, coaching with purpose, openly communicating expectations and being present.

For example, team members investing in their own and others, coaching, being present in all interactions and supporting each other to ensure we drive quality for our ultimate clients, meaning shareholders and wider stakeholders.

Everyone within our Audit practice is expected to demonstrate the Audit behaviours. We’ve embedded them into everything we do, including in our training and how we evaluate performance. We undertake an annual Audit Culture and Behaviours survey to measure how our people are experiencing the behaviours and identifying any barriers to demonstrating them. By taking the pulse of the practice and tracking our progress in embedding the behaviours, we can further develop and tailor our cultural programme. Our 2021 survey showed:

This is a modal window.

We asked some of our Culture champions to share their perspectives on our critical few behaviours.

View TranscriptThe firm aims to recruit, train, develop and retain the best and the brightest staff who share in our strong sense of responsibility for delivering high-quality services.

Our PwC Professional career progression framework underpins a training curriculum that provides a wealth of opportunities for our people to develop. An individual’s development journey starts when they join the firm and continues throughout their career, tailored to their grade, role and experience.

Training our auditors through a combination of remote access training and classroom training (pre-COVID) remains a key part of our quality assurance activities.

This year, our External Auditor Training (EAT) programme was redesigned for virtual delivery. During 2020 close to 3,400 individuals completed the EAT programme, attending the summer and autumn events virtually.

The topics covered in 2020 included effective project management, common pitfalls in financial statements review, auditing the future and auditors’ reporting requirements. Subject matter experts shared lessons learnt from investigations, and there was a dedicated session on developing a “forensic mindset”. Teams also spent time together focused on coaching, supervision and review, especially in the context of a hybrid working environment.

Performance is defined for our people as “what you do (your contribution and the impact it has) and how you do it (the behaviours you demonstrate)”. Managing contribution, impact and behaviours is a year round activity. All of our people have regular meetings with their career coach to discuss their ongoing performance.

Alongside the goals that all staff set for themselves each year, our auditors are also required to set a goal specifically relating to Audit Quality. These:

At the end of each performance year our auditors are evaluated against their goals (including their audit quality goals), the PwC professional career progression framework, and the Audit behaviours.

The Audit Partner Remuneration and Admissions Committee (APRAC) is a committee of the Audit Oversight Body (AOB). The APRAC supports the AOB in the oversight of specific obligations relating to the FRC’s objectives, outcomes and principles for operational separation.

The APRAC is comprised of up to three Audit Non Executives (ANEs). The APRAC’s primary responsibilities are:

The following documents provide further detail on matters relating to the firm's people agenda

We continue to invest in our Programme to Enhance Audit Quality (PEAQ) and are committed to performing consistently high quality audits. PEAQ is made up of four workstreams: structure and governance; culture and recognition; quality control activities; and supply and demand. Taken together these workstreams ensure our commitment to audit quality is reflected in everything we do.

The FRC’s Audit Quality Review team (AQR) undertakes inspections of the quality of the firm’s work as statutory auditors of public interest entities and aspects of the firm’s policies and procedures supporting audit quality.

The identification of a finding from an audit inspection means that a certain element of the audit has not, in the opinion of the reviewer, met the requirements of the relevant auditing standard. This does not mean that the audit opinion was wrong or that the financial statements were materially misstated. Of the audits inspected, 99% did not require a restatement of the financial statements.

Throughout the year to 30 June 2021, we also monitored 18 Audit Quality Indicators (‘AQIs’) ranging from engagement management to people metrics, on a quarterly basis to identify trends in audit quality. Separately to this, the Policy and Reputation Group (PRG) previously identified three people-related areas which could contribute to audit quality, and are measured through staff feedback surveys.

High quality audits support high quality corporate reporting and underpin trust in capital markets and among wider stakeholders. On average we identify at least five adjustments to each set of group financial statements we audit, with at least one of those adjustments being material to the financial statements. We also report any control deficiencies identified through our audit work to those charged with governance. On average we identify at least five key control findings per group audit.

The following documents provide additional background on the firm’s audit quality, and the system of quality management used to drive quality

PwC Audit methodology is a single, global methodology used by all PwC member firms. Based on International Standards on Auditing (ISAs), and adapted for supplementary UK requirements, it enables our engagements to scale from smaller and medium sized businesses to global enterprises.

Our methodology provides a framework for our engagements, and is tailored to each specific entity’s industry, circumstances and characteristics.

These downloads provide further detail on specific aspects of our methodology and audit approach

We established a separate Audit line of service on 1 July 2019. The Audit line of service’s revenues, split by public interest entity and non-public interest entity audits, is included in the financial information document that can be downloaded below. This document also includes the practice’s profitability as calculated by the Voluntary Code of Practice on Disclosure of Audit Profitability, issued by the Consultative Committee of Accountancy Bodies in March 2009.

Total revenues generated from Statutory audits and directly related services for all entities we audit

FY20: £754m

Audit revenues have increased this year, primarily resulting from scope changes arising from the continued impact that the COVID-19 pandemic is having on the organisations we audit. This increase in revenue allows us to deliver consistently high quality audits and meet the increasing societal and regulatory expectations of auditors.

The following documents provide additional information on the audit practice’s financial performance, its registrations, and other required disclosures